How COVID has Changed Drinking Behavior, Plus Pumpkin Beer Pull-Forward Data and New On-Premise Pricing Intelligence

Consumers are drinking earlier in the day, taproom visitor age demographics have shifted, and, yes, pumpkin beers are clearly now a summer option

In last month’s inaugural Untappd Insights newsletter, we examined data from past craft M&A to predict what the future holds for Stone following its acquisition by Sapporo.

This month, we refreshed data I presented at a Brewers Association Collab Hour last November on how COVID has fundamentally altered drinking behavior. We also explored Untappd check-in data to determine just how early the pumpkin beer season has shifted.

Before we dive in, I want to highlight that we’re releasing a super exciting On-Premise Pricing Intelligence product in September that uses aggregated menu data generated from nearly 20,000 Untappd for Business customers to provide real-time pricing insight. This tool allows users to filter by geography, venue type (bar, restaurant, etc.), brand, and container type/pour size to see the average price in a given geography as well as nationally.

For instance, as can be seen above, a pint of Stella Artois in California is about 9.5% more expensive (63 cents) than in the rest of the U.S. and about 5% less (38 cents) than a pint of Heineken in California. Increasingly relevant in this inflationary period, this is a great tool for brewers, distributors, and retailers to benchmark pricing in real-time across various geographies using a broad sample of data (generally several dozen to hundreds of predominantly independent retail venues in a given area). If you’d like to learn more, drop our team a line at contact@nextglass.co

COVID’S IMPACT ON DRINKING BEHAVIOR

I’ll continue to explore this topic throughout the rest of this year, but our current data suggests that COVID has fundamentally shifted some drinking behaviors.

Primary Drinking Window has Shifted Earlier

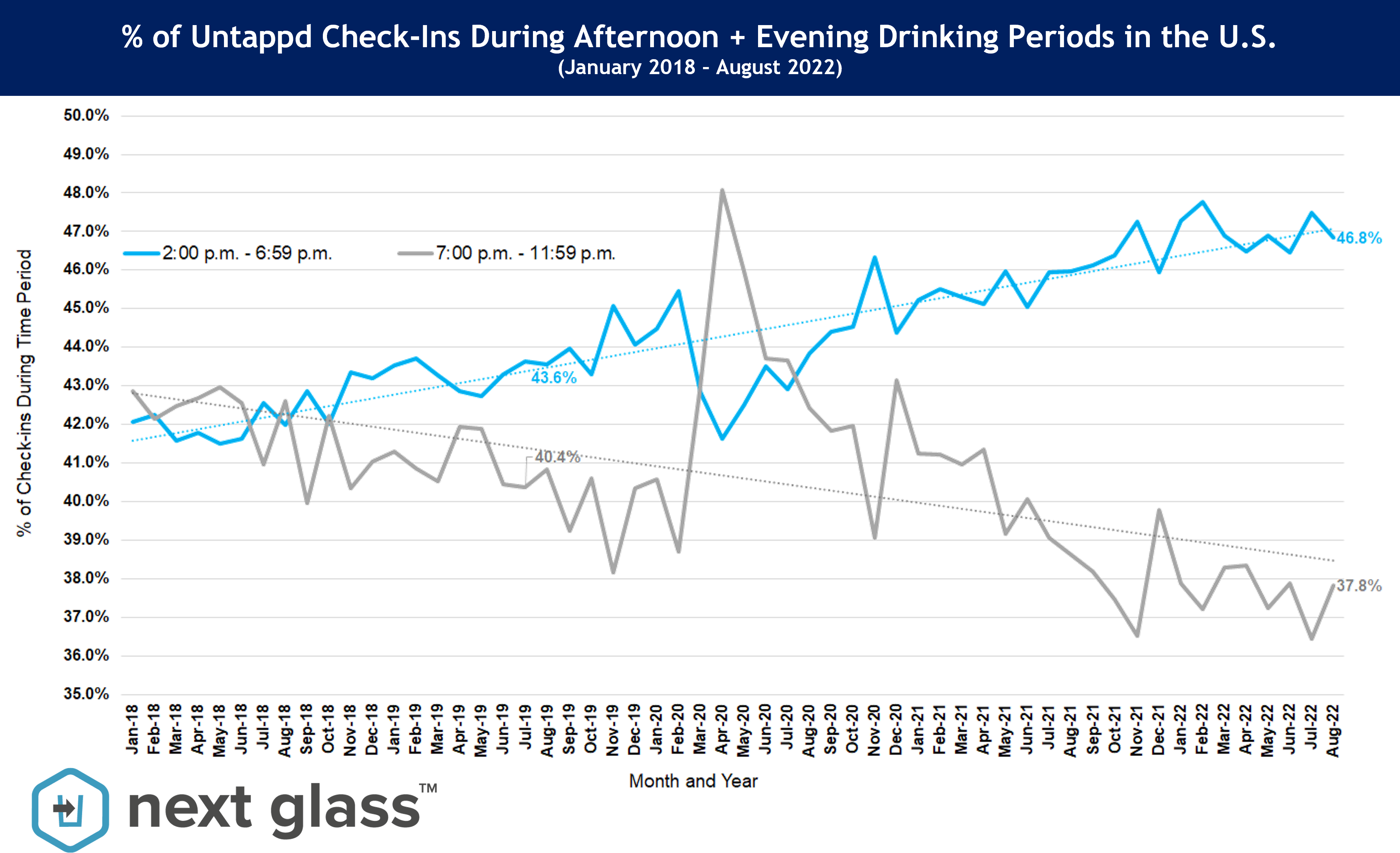

I’ve suspected that more work-from-home flexibility as well as a dramatic increase in the percentage of employees permanently working remotely would lead to earlier drinking occasions. Data from our Untappd users bears that out.

As can be seen in the graph above, the share of all Untappd check-ins in the U.S. generated in the 7:00 p.m. to midnight window has fallen from nearly 43% in January 2018 to 37.8% in August 2022. Where have those 5.2% of total U.S. check-ins gone? Primarily, they’ve shifted to 2:00 through 7:00 p.m. Whereas the percentage of total check-ins between the 2:00 p.m. and 7:00 p.m. range stood at just over 42% in January 2018 (less than the % occurring during the 7:00 p.m. to midnight period), check-ins during those hours stand at nearly 47% this month.

This shift is not simply explained by the 4:00 p.m. hour stealing massive share from the 5:00 p.m. hour. In fact, each one hour period beginning at 2:00, 3:00, 4:00, 5:00 and 6:00 p.m. saw a meaningful increase in check-in share while each one hour slot between 7:00 p.m. and midnight experienced a decrease in check-in share.

While the divergence in the percent of check-ins during these five-hour windows began prior to COVID, the data shows that the trend accelerated following the most severe of the 2020 lockdown measures. Interestingly, during the March 2020 - August 2020 when lockdown measures were most stringent, our users drank much later in the day. That immediately shifted and the trend towards earlier drinking resumed and accelerated when the on-premise reopened in most geographies in late-2020.

I believe a large factor in this paradigm shift to earlier drinking is workdays starting and ending earlier with more work-from-home flexibility and permanent remote work. Let’s be honest - it is much easier and socially acceptable now to wrap a Zoom meeting at 4:00, leave the basement office to head across the street to the neighborhood taproom, and manage the trickle of end-of-workday email from an iPhone than it was to start an early happy hour in 2019 when doing so meant leaving an office full of busy colleagues. Additionally, persistent staffing challenges have led many on-premise venues to shorten hours by way of earlier closures.

Taproom Share has Shifted from Millennials to Gen Z and Boomers

In the summer of 2021, during the Delta variant wave, a friend of mine mentioned that he was seeing far fewer families in the taproom than he had in pre-COVID times. His theory was that a meaningful number of parents weren’t willing to bring unvaccinated kids to taprooms at that time. We explored the data then (his hunch turned out to be true among our users) and refreshed it again to see if the trend had reversed or stabilized.

As the tables above illustrate, there has been a falloff in the percentage of check-ins generated at brewery taprooms by each 31-50 age grouping between 2019 and present day. In the U.S., the drop-off between 2019 and 2020 was most pronounced in the 31-35 and 36-40 age ranges. The downward trend in these age groups continued between 2020 and 2021 in both the U.S. and Europe.

In the U.S., the rate of decline seems to have slowed between 2021 and 2022 year-to-date, but the 31-35 and 36-40 age ranges in Europe have continued to decline meaningfully this year in terms of percent of overall check-ins generated.

Taking check-in share from the 31-50 crowd are younger drinkers—particularly Gen Zers under 25—and 50+ consumers. Check-ins generated at taprooms in the U.S. by Boomers and older Gen Xers have increased by nearly three full percentage points between 2019 and this year. In Europe, there has been a near 2.5x surge in taproom visitation by our users in the 18-25 age set between 2019 and 2022.

It will be interesting to revisit the data in 2023 with COVID even further in the rearview mirror to examine if behavior begins to revert to pre-pandemic levels.

THE GREAT PUMPKIN PULL-FORWARD

Inspired by this BeerAdvocate retweet from July 18th announcing that pumpkin beer season had arrived with Schlafly’s Pumpkin Ale arriving on grocery store shelves, our team decided to look at just how far forward pumpkin beer season has shifted in recent years.

While the data didn’t suggest that pumpkin beers have seen an increasing share of check-ins in July (the percent of pumpkin beer check-ins in July has held steady comfortably below 1.0%), I feel confident declaring that the official start of pumpkin beer season is now August. Pumpkin beers are clearly hitting the shelves and being consumed earlier in the year now than they were five years ago.

On the other hand, pumpkin beer season does not appear to have lengthened. Much of the shift to August appears to have drawn from November, meaning that while these gourd-inspired creations are being enjoyed earlier in the year, they’re also leaving the market earlier than in years past.

That’s all for August! In September, we’ll explore on-premise consumption shifts among bars, restaurants, and taprooms. In the meantime, if you find yourself thirsty for more pumpkin beer content, head over to Hop Culture and read yesterday’s “Are Pumpkin Beers ‘Squashed’ for Good?” piece.

Until next month, enjoy and check-in your beers!

CEO, Next Glass