What Untappd Data From Previous California Craft Acquisitions Tells us About Stone's Future

Data following the acquisitions of Lagunitas, Ballast Point, and Golden Road by mega-brewers points to softened consumer sentiment but rapid retail growth for Stone.

“Death, taxes, and venerable California craft breweries being acquired by mega-brewers.” Or so the saying goes.

Since late-2015, the M&A fault lines beneath the California craft beer scene had been relatively still. In September of that year, AB InBev acquired Golden Road and Lagunitas secured investment by Heineken for 50% ownership (which led to an eventual complete takeover in May 2017), followed in quick succession by Constellation Brands’ acquisition of Ballast Point in November.

But this summer, the tectonic plates started to shift again. On June 24th, it was announced that Stone had been acquired by Sapporo for $165 million.

Using data from millions of Untappd check-ins (a check-in is a consumption moment logged by an Untappd app user) on the pre- and post-acquisition periods for the three California breweries, we can predict what’s coming down the line for Stone.

CONSUMER SENTIMENT

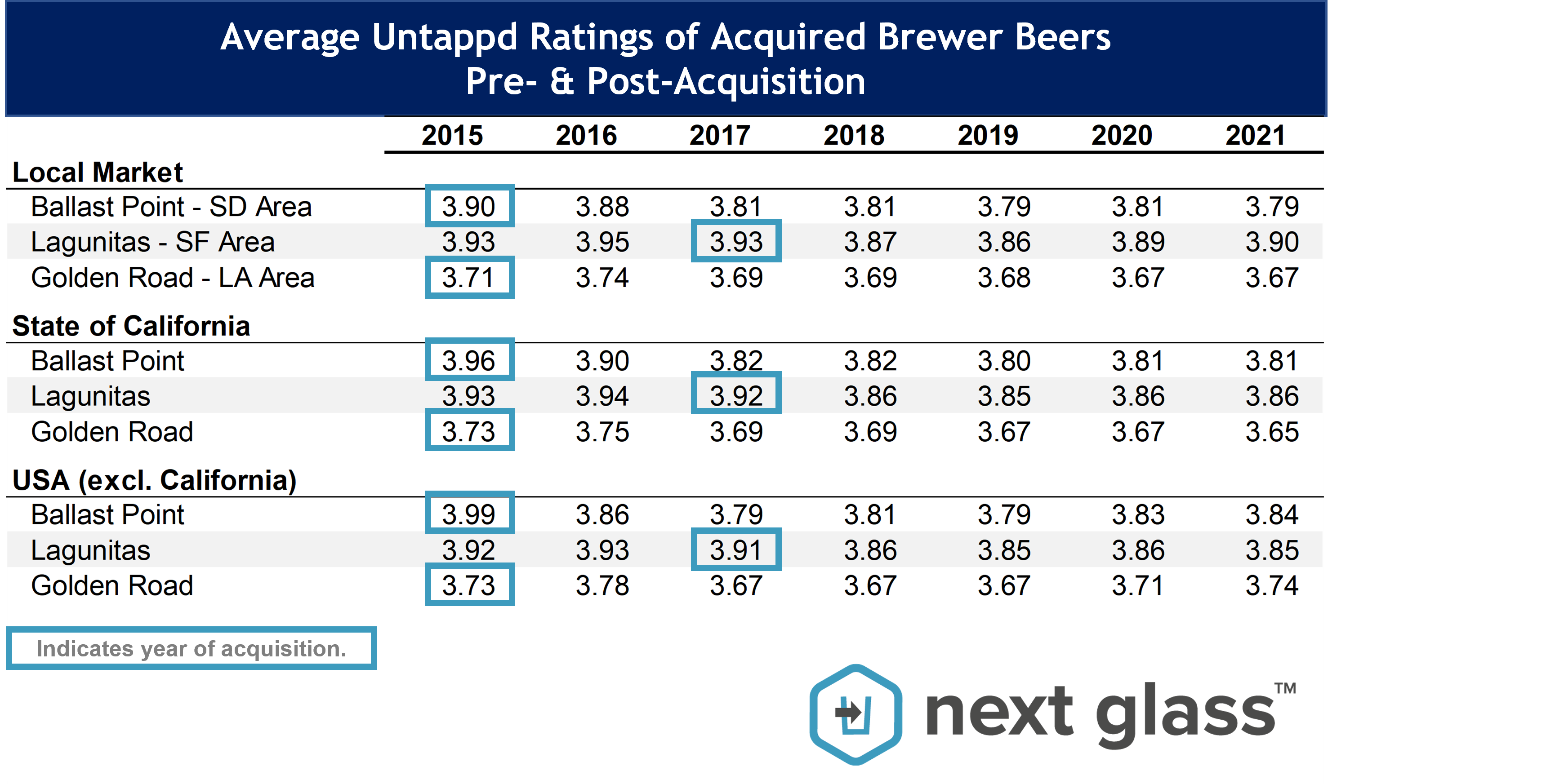

Let’s start with consumer sentiment. Fair or not, a craft brewer selling to a mega-brewer attracts criticism from ardent craft consumers. But how does such a transaction play out across a broader subset of consumers on Untappd, who rate beers on a 0.00 to 5.00 scale in quarter-point increments? To get a sense for this, we can look at the pre- and post-acquisition ratings of the three California craft breweries that were acquired or received a meaningful investment (in the case of Lagunitas) in 2015. As can be seen in the table below, there are clear local, statewide, and national impacts when comparing average ratings for each brewery’s beers prior to and following acquisition.

The prevailing narrative around these acquisitions tends to be that local consumers, like fans of fledgling indie bands that make it mainstream, sour on these brewers upon acquisition. Our data suggests that, while noticeable, the fall-off is not as severe as the noise from the Twitterati might lead the market to believe. As the table above illustrates, Ballast Point, Lagunitas, and Golden Road experienced a clear but far from catastrophic drop in average rating in their local markets – San Diego, San Francisco Bay Area, and Los Angeles, respectively – as well as in their shared home state of California in the years following their transactions.

Ballast Point’s average rating has suffered the most of the trio, dropping locally in San Diego over a full tenth of a point on Untappd’s 5.00 point rating scale and 0.15 points in California from its pre-acquisition period in 2015 to 2021. Lagunitas and Golden Road both also experienced modest average rating decreases in their home markets and statewide in California over the same period. Interestingly, the average rating for Lagunitas products actually increased in each geographic classification following its investment from Heineken but dropped in each area after Heineken fully acquired the Petaluma, CA-based brewery in 2017.

Brand perception of highly-regarded craft breweries seems to suffer nationally in the wake of these transactions. In the social media/late-Web 2.0 era, the brand cachet associated with beloved brewers is no longer locally controlled - breweries are followed globally on Instagram, Untappd, BeerAdvocate, and, to an increasingly alarming degree, even TikTok. The local Indie band brewery now has 100,000 Instagram followers diffused globally and word of these deals travels well beyond the local business journal (just ask your social media manager to check the comments!). However, it's worth noting that in Golden Road’s case, although starting off a lower average rating of 3.73 compared to figures above 3.90 nationally for Ballast Point and Lagunitas, its average rating is actually now higher across the 49 non-California states than it was prior to be being acquired (this is known as the Mango Cart Effect.)1

DISTRIBUTION GROWTH

In terms of growth into retail outlets, each of the three breweries grew very quickly between 2016 and the end of 2019 (although Ballast Point had already topped out in 2017 and was shrinking in retail venue footprint in 2018 and 2019 prior to Constellation’s divestiture to Kings & Convicts in 2020).

As indicated in the graph below, Ballast Point (+47%), Lagunitas (+26%), and Golden Road (+116%) all grew seemingly overnight into new retail venues in 2016, each of their first full years beneath corporate parents with broader distribution reach. While Ballast Point and Lagunitas essentially stabilized after torrid year one growth, the Red Network continued to grow Golden Road’s reach in each successive year pre-pandemic. By 2019, Golden Road received check-ins at 5.3x as many retail venues (14,219) as it had in the one year prior to its acquisition (2,679). And, while Ballast Point and Lagunitas already enjoyed national distribution pre-COVID, Golden Road has grown from 3 states with >500 check-ins (indicating probable distribution into that state) pre-acquisition to 36 today.

How about Heineken’s efforts to spread Lagunitas throughout Europe? I recall vividly a pervasive Lagunitas presence on a 2018 work trip to The Netherlands and London. Seemingly every Heineken-owned or tied pub had Lagunitas on offer. The data bears out what I saw. In 2015, we only saw Lagunitas brands show up in 2,482 venues in Europe. By 2019, that number had increased to 9,401, nearly 4x growth. Lagunitas brands now receive >500 check-ins annually in 22 countries (vs. 11 in the pre-acquisition period).2

Heineken clearly had success introducing Lagunitas brands into new geographies as well as to new venues in nascent and pre-existing markets in Europe. Will Sapporo do the same with Stone? Only time will tell, but the formula for introducing a highly-regarded California craft brand into new overseas markets certainly seems to have worked for Heineken.

So, what’s my prediction for Stone? While past performance doesn’t guarantee future results, it’s generally the best indicator. And I expect the same to be true in the case of California brewery M&A. With an impressive 3.88 average rating across all of its beers today, Stone’s domestic consumer sentiment will almost assuredly decrease. I suspect its average rating in San Diego, across California, and nationally will dip about a tenth of a point over the next two years and settle to an average between 3.75 and 3.80. Only Sapporo knows what is planned for distribution, but our data found Stone beers in 26,483 retail venues worldwide and receiving >500 check-ins annually in 30 countries. I’d bet Sapporo leverages its international distribution and increases Stone’s reach to roughly 35,000 retail locations in the next two years (just shy of a 1.4x increase).

Oh, and one last prediction: we won’t wait another half-decade for a California craft institution to be acquired by a mega-brewer (or might the next domino fall to an acquisitive non-alc player?).

If you’re interested in learning more about how our data can work for you, please don’t hesitate to reach out! And of course, please reach out with suggested topics, feedback, and questions.

Cheers!

Trace Smith

CEO, Next Glass

trace@nextglass.co

Golden Road’s Mango Cart accounts for nearly 20% of all of the brewery’s check-ins and maintains an impressive 3.8 average rating, a clear case of a brewery’s most popular beer boosting its overall rating.

Lagunitas has been checked-in at least once in 120+ countries in the last twelve months but received >500 check-ins in 22 countries.